ADR Cycles in the U.S. Hotel Industry

By: Hans Detlefsen, Carter Wilson, and Hannah Smith

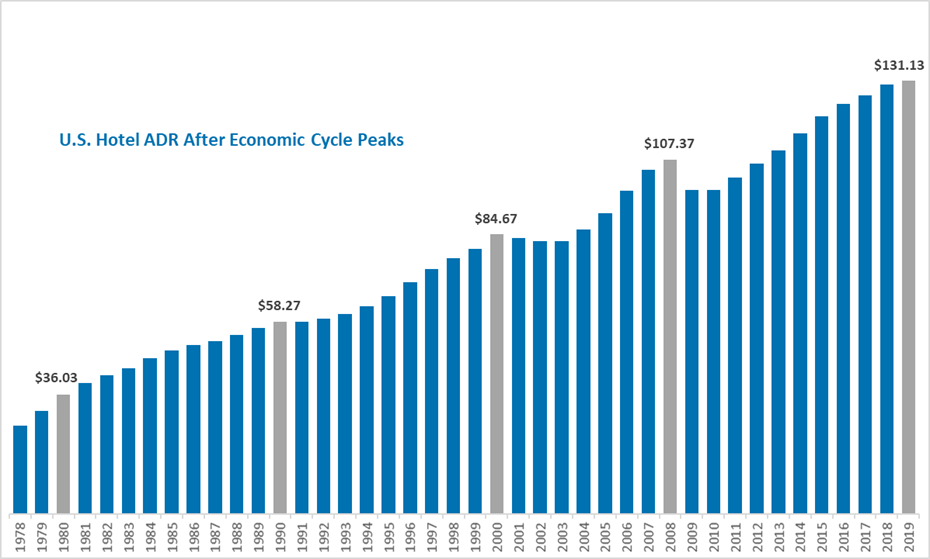

Hotels always recover from economic downturns, right? Wrong. It is true the U.S. hotel industry, in aggregate, has always rebounded from past recessions. But this trend masks the fact that each cycle has winners and losers. Many hotels never recover. The U.S. hotel industry, on whole, has set new records for total revenue and ADR in each historical economic cycle since this data has been collected . The following figure illustrates this upward trend, showing aggregate U.S. hotel ADRs achieving new peaks in each of the past five economic cycles.

FIGURE 1 – AGGREGATE ADR ALWAYS RECOVERS

Sources: STR and HA&A

However, many individual hotels never recover after a recession. During the past economic cycle, approximately 1 in 10 U.S. hotels never rebounded to the ADR levels they achieved in 2008. During the Great Recession of 2009, aggregate ADRs declined significantly in the U.S. But by 2013, the industry had achieved a new ADR peak. But this recovery in aggregate performance obscures the fact that approximately 10 percent of U.S. hotels never recovered to their prior ADR peaks, even by 2019. We expect a similar outcome following the current pandemic and economic recession of 2020.

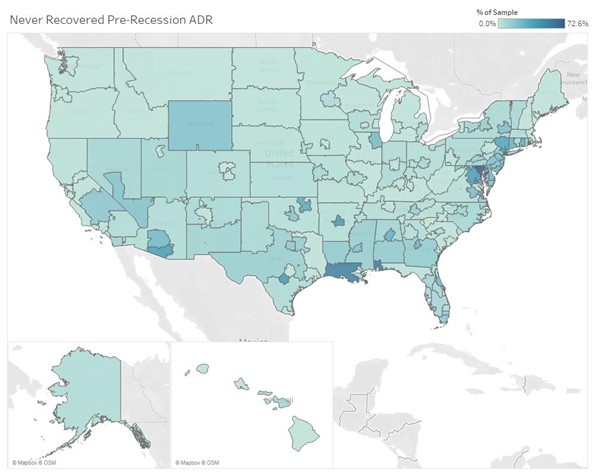

Hotel Appraisers & Advisors (HA&A) collaborated with STR to evaluate 7,530 U.S. hotels that maintained the same brand and chain scale during the U.S. economic cycle spanning from the 2008 peak through the subsequent peak in 2019. Of this sample, 6,785 hotels recovered to their nominal 2008 ADR peak levels by 2019. However, 745 hotels in our sample never got back to their peak ADR levels, even in nominal dollars.

The failure of some hotels to recover during the past economic cycle was not limited to any single region. All regions of the country had some hotels that never recovered. The following figure shows a map of where the non-recovered hotels are located throughout the U.S. In this map, darker shades of green indicate market areas with higher percentages of hotels that did not recover during the past economic cycle.

FIGURE 2 – HOTELS CAN FAIL IN ALL REGIONS

Source: STR

All regions of the U.S. have hotels that failed to recover. During the past cycle, some market areas such as Baltimore, New Orleans, Tucson, and San Antonio had relatively higher instances of hotels that did not recover. Several factors including business relocations, natural disasters, sociopolitical instability, and supply growth may have contributed to these performance trends.

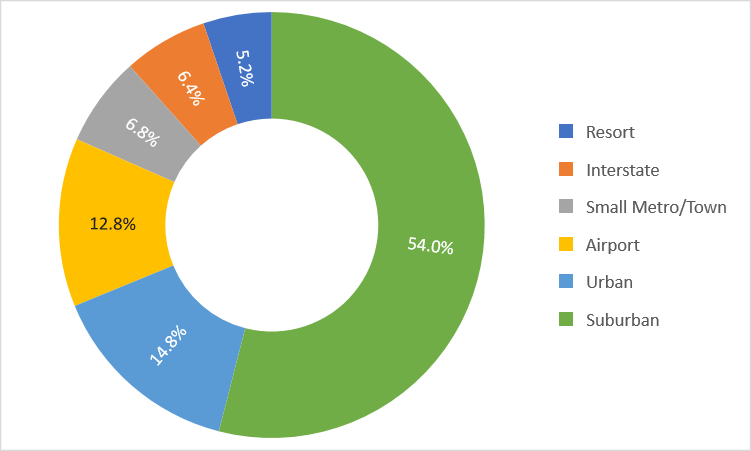

A hotel’s specific location within a market can affect whether it recovers from an economic downturn. Suburban locations appear to be, by far, the riskiest type of hotel location in terms of business cycle risk. We observed six location categories. Suburban locations accounted for more than half of all the hotels that never recovered to their prior ADR peaks. All five remaining location categories, combined, accounted for the remaining 46 percent of non-recovered hotels. The following figure illustrates the distribution of these non-recovered hotels by location type.

FIGURE 3 – SUBURBAN LOCATIONS APPEAR MOST RISKY

Sources: STR and HA&A

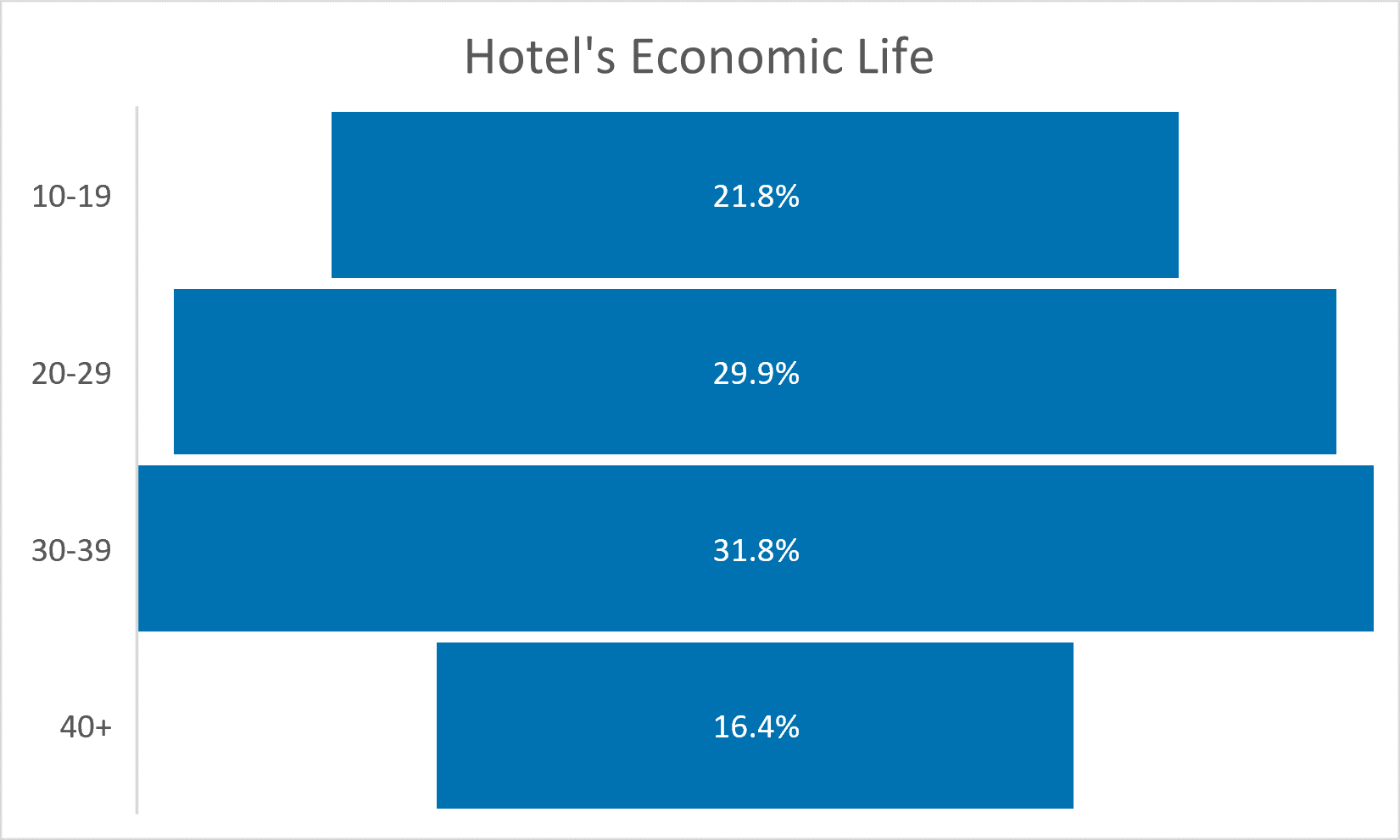

The age of a hotel matters. Age can affect which hotels are likely to be the winners and losers in each economic cycle. The greatest concentration of non-recovered hotels had building ages of 30-39 years old. The following figure shows the distribution of non-recovered hotels by age category in the United States.

FIGURE 4 – RISK INCREASES AS HOTELS APPROACH AGES 30 AND 40

Sources: STR and HA&A

This data supports anecdotal evidence that many hotel owners renew their franchises after the initial 20-year terms, often for an additional 10-20 years. For example, suppose a hotel owner renews her Hampton Inn & Suites franchise agreement for an additional 20 years after an initial 20-year term. During the final 10 years of the extension, as the building approaches its 40th birthday, the owner may determine that getting another franchise extension will be unlikely or cost prohibitive. This is especially true since the hotel is already over 30 years old and may feature some functional obsolescence. The owner may then decide to stop investing in the property beyond the bare minimum needed to meet brand standards.

Such properties are nearing a period when they will likely “de-flag” to a lower chain scale, or independent brand. But even while benefiting from its original brand, performance may start declining as the property’s deferred maintenance and functional obsolescence make it increasingly less competitive in its market. While this example is hypothetical, it reflects the experience of many real hotels. It is also consistent with previously published data in which one of the authors estimated the median economic life of economy hotels in the United States was approximately 39 years.

The findings from this research support several conclusions relevant to hotel investors and appraisers.

- Roughly 10 percent of hotels never recover from economic recessions in a typical business cycle. Heavy consideration of the factors determining winners and losers in the U.S. hotel industry should be part of any hotel investment strategy.

- Suburban hotels may have inherent risks related to relatively rapid changes in development trends experienced in some suburban markets.

- Hotels nearing the termination of a renewed franchise period may represent a greater risk than hotels within their initial franchise terms or at the beginning of a renewed term.

- Markets affected by natural disasters, sociopolitical instability, or supply shocks can experience declines that prevent large numbers of hotels from recovering to prior peaks.

- Hotels in markets that experience developments of same-brand competitors can be subject to heightened supply risk not understood by many investors. Cities like Austin, Chicago, Denver, Indianapolis, and San Antonio are good illustrations of this phenomenon. Newer Courtyard, Hampton Inn, and Residence Inn brands were duplicated in these downtown markets.

In general, the U.S. hotel industry is robust and historically has always rebounded from any recession or shock to performance. Every cycle’s peak ADR has been surpassed by a new peak in the following business cycle. However, by definition, some individual hotels will not fare as well as the average hotel. Winners and losers emerge after each business cycle. The authors hope this article helps to illustrate some ways that industry participants can evaluate hotel investment risks.